Essential points: Behavior is the engine of financial well-being, driving your actions, shaping outcomes, and turning knowledge into impact. This article explores how financial behaviors interact with both resources and psychology, completing the trifecta of holistic well-being. You’ll uncover how habits form, why they stick, and what influences them, from personal values to economic conditions. Packed with practical strategies for replacing harmful habits with helpful ones, it reveals the transformative power of budgeting, saving, investing, and goal-setting. By mastering the behavioral dimension, you unlock the ability to align your money moves with your values, reduce financial stress, and build resilience over time.

Imagine if every swipe of your credit card, every bill you pay, and every dollar you save was a step towards your ideal financial future. Sounds too good to be true? Welcome to the power of financial behaviors, the often-overlooked superheroes of your money story.

In this final installment of our financial well-being series, we’re pulling back the curtain on the actions that can make or break your financial dreams. You’re about to discover how small, consistent financial behavior changes can lead to big wins, and why your daily money habits are the secret ingredient to lasting financial success.

Ready to turn your financial knowledge into action and your goals into reality? Let’s dive into the world of smart money moves and behavior hacks that will transform your financial life.

Gearing Up: A Quick Refresher

Here’s a brief recap in case you haven’t read Part 1, The Currency of Well-being: Navigating Your Financial Resources, or Part 2, The Emotional Ledger: Balancing Mind and Money, of this series.

Of all the definitions of financial well-being out there, one of the most common is feeling confident and content with your current financial standing and future prospects.

Financial well-being is important because it touches on the other aspects of overall well-being. A lack of financial wellness can undermine physical, emotional, social, occupational, and other essential dimensions of life.

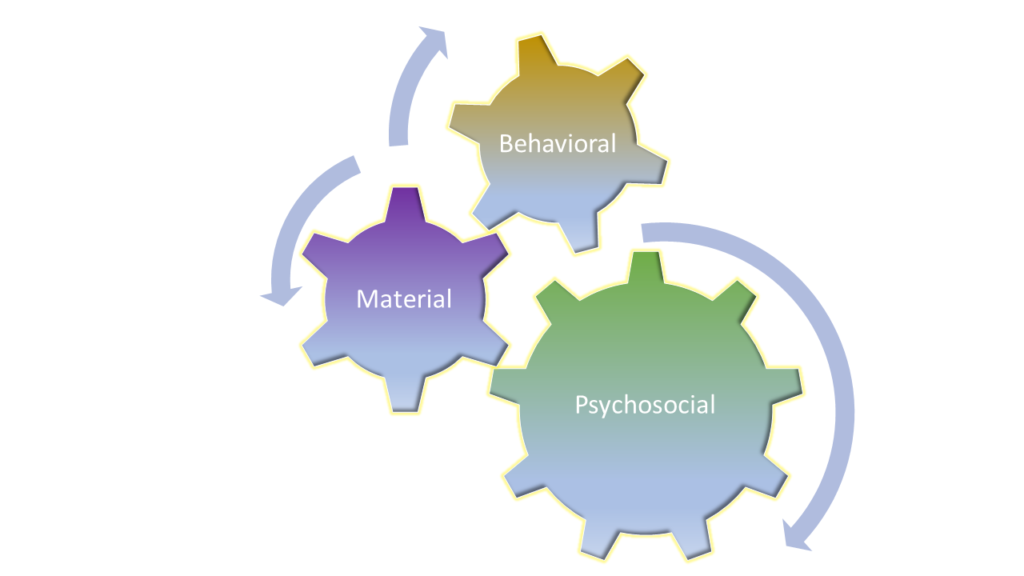

Imagine your financial well-being is a machine, with three components linked up like gears in motion. These gears represent the material side of your well-being (your resources such as your home or savings), the psychosocial side (your cognitive, emotional, and interpersonal responses to your financial situation), and the behavioral side (the actions you take to meet your financial obligations).

Just as synchronized gears power a machine, your material resources, psychosocial factors, and financial behaviors work in tandem to drive your comprehensive financial well-being.

We explore all these domains in our 3-part series. But this post focuses on the third domain: behavioral.

What Is Financial Behavior?

Although there’s no universal agreement on a definition of financial behavior, this term can be used to describe “any actions or conduct related to the management of money.” Financial behaviors encompass the decisions, habits, and practices individuals and households engage in when it comes to earning, spending, saving, borrowing, and investing their financial resources.

These financial behaviors can have a powerful impact on your overall financial well-being and stability. They’re the tangible manifestations of your financial knowledge, attitudes, and beliefs, the ways in which you put your financial understanding into real-world practice. Examining and understanding these behaviors is crucial for developing effective strategies to improve long-term financial outcomes.

How Do Financial Behaviors Interact with Financial Resources and Psychology?

To understand the part behavior plays in holistic financial well-being, it’s useful to look back to the gears analogy, where behavior interacts with financial resources and psychosocial factors. These three parts are deeply interconnected, each influencing and being influenced by the others in a continuous cycle.

The interplay between these elements creates a dynamic system where changes in one area can have ripple effects throughout your financial life. For instance, adopting positive financial behaviors can lead to increased resources, which in turn can positively impact your psychological relationship with money. On the other hand, negative behaviors can deplete resources and create psychological stress, potentially leading to further detrimental behaviors.

The Behavior-Resource Connection

Outside structural inequities in society and certain circumstances beyond your control, your financial resources are determined by your financial behaviors: the work you do; your spending, saving, and investing activities; and your personal protection practices (insurance and estate planning).

These behaviors directly impact the accumulation, preservation, and growth of your financial resources. For example, consistent saving behavior can build an emergency fund, while responsible investing can grow wealth over time. On the other hand, overspending or neglecting financial planning can erode resources, regardless of your income level.

Understanding this connection empowers you to make informed choices that align your behaviors with your financial goals, potentially leading to improved management of your resources and better financial well-being.

The Behavior-Psychosocial Connection

The psychosocial dimension includes:

- your beliefs about wealth

- how you feel when dealing with money matters

- the influence of your family, culture, and friends on your financial attitudes

It’s the set of lenses through which you view your financial world, often coloring your decisions and behaviors without you even realizing it. The consequences of these decisions and behaviors affect you financially.

While psychosocial factors affect your finances, the reverse is also true. Your finances affect your thoughts, feelings, and social environment. These influences come in the form of such reactions as insomnia over making ends meet, feelings of hopelessness over debt, and arguments with your partner over family finances.

This bidirectional relationship between behavior and psychology creates a feedback loop that can either reinforce positive financial habits or perpetuate negative ones. Recognizing this connection is crucial for developing strategies to improve financial behaviors and, by extension, overall financial well-being. It underscores the importance of addressing both the practical and emotional aspects of personal finance to achieve lasting positive change.

How Do Different Behaviors Help or Harm Our Finances?

Common Positive Financial Behaviors

Cultivating these positive financial behaviors can significantly enhance your overall financial well-being:

1. Budgeting and tracking expenses: This foundational habit provides a clear picture of your cash flow, helping you make informed decisions about spending and saving. By knowing where your money goes, you can identify areas for improvement and align your spending with your financial goals.

2. Regular saving and investing: Consistently setting aside money for the future builds financial security and opens up opportunities for wealth growth. Whether it’s an emergency fund or long-term investments, this behavior helps you prepare for both unexpected events and future aspirations.

3. Paying bills on time: Timely bill payment not only avoids late fees and interest charges but also helps maintain a good credit score. A strong credit history can lead to better loan terms and financial opportunities in the future.

4. Comparison shopping and researching before major purchases: This behavior ensures you get the best value for your money. By taking the time to research and compare options, you can make informed decisions that balance quality and cost, potentially saving significant amounts over time.

5. Continuous financial education: Staying informed about personal finance topics helps you adapt to changing economic conditions and make better financial decisions. Whether through reading, courses, or seeking professional advice, ongoing learning empowers you to take control of your financial future.

By incorporating these positive behaviors into your financial routine, you create a strong foundation for long-term financial well-being. Remember, small, consistent actions can lead to significant improvements over time.

Common Negative Financial Behaviors

Certain activities and decisions can be detrimental to your financial and holistic wellness:

1. Impulse spending: Impulsive and compulsive buying patterns can quickly drain a budget and cause you to forfeit your financial security and dreams for momentary entertainment or relief from difficult emotions. By distinguishing between needs and wants, practicing mindfulness about spending, and bringing your spending into alignment with your values, you can achieve deeper, longer-lasting satisfaction.

2. Neglecting to save or invest: Life is unpredictable, and no one knows when unexpected events like an auto or appliance breakdown, a major illness, or unemployment will happen. Having an emergency fund makes it easier to ride out these situations instead of taking out high-interest loans or resorting to other desperate measures. Saving and investing are also important for funding dream vacations, college tuition, early/comfortable retirement, and other financial goals that enhance quality of life.

3. Overuse of credit: Excessive use of credit can pave the way for long-lasting financial challenges, including mounting debt, accumulating fees, and a compromised credit score. When you lean too heavily on credit or use it without intention, you risk taking on unsustainable levels of debt. If left unchecked, overuse of credit may end in severe consequences like bankruptcy, eroding your overall financial health and well-being.

4. Avoiding financial planning: Failing to have a financial plan can lead to overspending, an uncertain financial picture, and the absence of a basis to make informed decisions. It can also result in a lack of control and direction, which can ultimately lead to financial distress or failure.

5. Ignoring financial statements or bills: This behavior can cause you to:

- Miss fraudulent activity on your account

- Incur fees due to overdrafts or late charges

- Overlook missed payments and other errors

- Be unaware of rate increases

- Damage your credit rating due to late payments and accounts that go to collections

A low credit rating, in particular, can have severe and lasting consequences. The interest rates you pay on loans are typically higher, and prospective employers can (with your consent) legally check your credit report as part of the hiring process in most of the United States. So staying on top of financial statements is vital to your financial wellness.

What Influences Financial Behaviors?

Financial behaviors don’t develop in isolation. They’re shaped by a complex interplay of internal and external factors. From our personal beliefs to the world around us, numerous elements contribute to how we manage money. Understanding these influences can provide valuable insights into our financial decision-making processes and help us make more informed choices. Let’s explore the key factors that play a role in shaping our financial behaviors.

Personal Values and Goals

Your personal values and goals play a crucial role in shaping your financial behaviors. These deeply held beliefs and aspirations serve as a compass, guiding your decisions about earning, spending, saving, and investing. For instance, if you highly value financial security, you’re more likely to prioritize saving and building an emergency fund. Similarly, if one of your main goals is early retirement, you might be more inclined to aggressively invest in your 401(k) or other retirement accounts.

It’s important to regularly reflect on your values and goals, as they can change over time. As you progress through different life stages, your priorities may shift, impacting your financial behaviors. By aligning your financial decisions with your current values and goals, you can ensure that your actions are in harmony with what truly matters to you, leading to greater financial satisfaction and well-being

Social and Cultural Influences

The society and culture you’re part of can significantly influence your financial behaviors. Family traditions, peer pressure, and societal norms all play a role in shaping your attitudes towards money and your financial habits. For example, if you grew up in a culture that emphasizes frugality, you might be more inclined to save and avoid unnecessary spending. Conversely, if your social circle places a high value on material possessions, you might feel pressure to spend more on luxury items or experiences.

Media and advertising also contribute to these social and cultural influences. The constant bombardment of marketing messages can shape your perceptions of what’s normal or desirable in terms of spending and lifestyle. Being aware of these influences can help you make more conscious financial decisions that align with your personal values rather than external pressures.

Economic Environment

The broader economic environment in which you live and work has a profound impact on your financial behaviors. Factors such as inflation rates, interest rates, job market conditions, and overall economic growth or recession can influence your decisions about saving, spending, and investing. For instance, during periods of high inflation, you might be more inclined to invest in assets that can keep pace with rising prices. In a robust job market, you might feel more confident about taking on debt or making major purchases.

Understanding the current economic climate and its potential impact on your financial situation is crucial. By staying informed about economic trends and indicators, you can make more informed decisions about your money. This might involve adjusting your investment strategy, reassessing your career plans, or modifying your spending habits in response to changing economic conditions.

Financial Literacy and Education

Your level of financial literacy and education plays a significant role in shaping your financial behaviors. The more you understand about personal finance concepts, investment strategies, and money management techniques, the better equipped you are to make sound financial decisions. Financial literacy can help you avoid common pitfalls, such as high-interest debt or unsuitable investments, and empower you to take advantage of opportunities to grow your wealth.

Investing in your financial education is an ongoing process. As financial products and regulations evolve, it’s important to stay up-to-date. This might involve reading personal finance books, attending workshops, or seeking advice from financial professionals. By continually expanding your financial knowledge, you can develop more effective money habits and strategies that contribute to your long-term financial well-being.

Past Experiences with Money

Your past experiences with money, both positive and negative, can significantly influence your current financial behaviors. If you’ve experienced financial hardship in the past, such as job loss or overwhelming debt, you might be more cautious with your spending and prioritize building an emergency fund. On the other hand, if you’ve had success with certain investments or financial strategies, you might be more inclined to continue those practices.

It’s important to reflect on your money history and understand how it shapes your current attitudes and behaviors. While learning from past experiences is valuable, it’s also crucial to recognize when past events might be holding you back from making beneficial financial decisions in the present. By consciously examining your money history, you can work to overcome any limiting beliefs or behaviors and develop a healthier, more balanced approach to your finances.

What Is the Role of Habits in Financial Behaviors?

Habits are the invisible architects of our financial lives. These ingrained patterns of behavior, often operating beneath our conscious awareness, significantly shape our money management practices. Understanding the role of habits in financial behaviors is crucial, as they can either propel us toward financial success or hinder our progress. By examining how habits form, influence our financial well-being, and can be changed, we gain powerful tools for improving our financial health.

Over Time, Habits Make Behaviors Automatic

Financial habits, like any other habits, develop through repetition and reinforcement. When you consistently perform certain financial behaviors, such as regularly setting aside money for savings or checking your account balances daily, these actions become automatic over time. This process occurs in your brain as neural pathways are strengthened, making it easier and more natural to repeat these behaviors.

Your environment plays a crucial role in habit formation. If you grow up in a household where budgeting is a regular practice, you’re more likely to adopt this habit yourself. Similarly, the tools and systems you use can facilitate habit formation. For instance, setting up automatic transfers to your savings account can help establish a saving habit without requiring constant conscious effort.

Ingrained Habits Impact Financial Well-being

Ingrained financial habits can have a profound impact on your overall financial well-being, either positively or negatively. Positive habits, such as living below your means, regularly contributing to retirement accounts, or maintaining a good credit score, can compound over time to significantly improve your financial situation. These habits work in your favor, often without you having to think about them consciously.

On the flip side, negative financial habits can be equally powerful but detrimental to your financial health. Habits like impulse buying, relying on credit cards for everyday expenses, or neglecting to track your spending can lead to debt accumulation and financial stress. The challenge with ingrained habits is that they can be difficult to recognize and even harder to change, as they often operate below the level of conscious awareness.

Unwanted Financial Habits Can Be Replaced with New Behaviors

Changing ingrained financial habits requires conscious effort and a strategic approach. The first step is to identify the habits you want to change. This might involve tracking your spending, analyzing your financial behaviors, or seeking feedback from a trusted friend or financial advisor. Once you’ve identified the habits you want to modify, you can begin the process of change.

One effective strategy is to replace negative habits with positive ones. For example, if you have a habit of impulse buying, you might replace it with a habit of adding items to a wish list and waiting 24 hours before making a purchase. Another approach is to use triggers and rewards to reinforce new habits. You could set up a reminder on your phone to review your budget weekly and reward yourself with a small treat when you stick to it consistently.

It’s important to remember that habit change takes time and patience. Start with small, manageable changes and gradually build on your successes. Celebrate your progress along the way, and don’t be discouraged by occasional setbacks. With persistence and the right strategies, you can reshape your financial habits to support your long-term financial well-being.

Why Is Behavior Important to Financial Well-Being?

Your behavior with money plays a large role in determining your financial position and financial stability. The ways you act in response to situations can either support or hinder your ability to meet your financial obligations and pursue a lifestyle that aligns with your values and goals.

Your positive behavior with money impacts your financial and overall wellness. Taking the right action will allow you to:

- Implement Financial Knowledge. While financial knowledge is important, knowledge alone doesn’t improve financial situations; it’s the consistent application of that knowledge through actions (behaviors) that leads to the real changes you wish to see in your finances.

- Form Good Financial Habits. Repeated positive financial behaviors become habits, making good financial management more automatic and sustainable over time.

- Achieve Financial Goals. Financial goals are realized through a series of behaviors and actions taken over time. While desire and planning are vital to achieving goals, they must be accompanied by effective behavior.

- Overcome Psychological Barriers. Behaviors can help bridge the gap between intentions and actions, overcoming psychological obstacles like procrastination or fear.

- Develop Adaptability and Financial Resilience. Financial behaviors allow you to adapt to changing circumstances and unexpected events, contributing to long-term financial resilience.

- Compound Results Over Time for Greater Impact. Small, consistent behaviors (like investing or paying down debt) can have a significant cumulative impact on financial well-being over time.

- Reduce Stress. Positive financial behaviors can lead to a greater sense of control and reduced financial stress, improving overall well-being.

- Have Tangible Effects. Behaviors can transform abstract financial concepts into practical results in your life.

- Provide Valuable Feedback. Behaviors provide concrete feedback on financial strategies, allowing for adjustment and improvement over time.

- Serve as a Model of Positive Behavior for Others. Good financial behaviors can positively influence others, especially family members, creating a broader impact on financial well-being.

What Are Key Financial Behaviors?

A few key practices stand out as the building blocks that shape your financial health and future. These behaviors form the foundation of sound money management, helping you navigate the complex world of personal finance. By mastering these essential financial behaviors, you can take control of your financial life, build wealth, and work towards long-term financial security. Let’s explore the critical actions that can make a significant difference in your financial journey.

Budgeting and Tracking Expenses

Budgeting and expense tracking are the cornerstones of financial well-being. By creating a personal financial plan, you take control of your financial life, deciding in advance how to allocate your income toward essentials, savings, and discretionary spending. A budget empowers you to live within your means and helps you avoid the pitfalls of overspending. The point isn’t to restrict your spending; it’s to encourage informed choices that align with your financial goals.

Expense tracking complements budgeting by giving you a clear picture of where your money actually goes. By regularly monitoring your spending, you can spot patterns, identify wasteful habits, discover unused subscriptions, and make adjustments as needed. This practice helps you stay on track and ensures that your financial decisions support your long-term objectives. When you know exactly how you spend your money, you’re better equipped to make mindful decisions that enhance your financial security and peace of mind and, in doing so, support your overall wellness.

Saving and Investing

Saving and investing are vital behaviors that build your financial future. Regular saving creates a safety net, providing you with the resources to handle unexpected expenses without derailing your financial plan. It also helps you achieve your long-term goals, such as buying a home, funding education, or enjoying a comfortable retirement. The key is to make saving a habit, treating it as a non-negotiable part of your budget.

Investing takes your savings a step further by allowing your money to grow over time. When you invest, you put your money to work, potentially earning returns that outpace inflation and increase your wealth. Whether you choose stocks, bonds, mutual funds, or real estate, investing requires careful planning and a long-term perspective. By committing to regular saving and smart investing, you’re actively securing your financial future and ensuring that your money contributes to your holistic well-being in the best possible way.

Managing Debt

Effective debt management is crucial for maintaining financial health. Debt, if not managed wisely, can quickly spiral out of control, leading to stress and financial strain that undermine your overall well-being. The key to successful debt management is understanding your obligations and creating a plan to pay them off as efficiently as possible. This may involve prioritizing high-interest debt, consolidating loans, or negotiating with creditors for better terms.

Paying down debt not only reduces financial pressure but also frees up resources that can be redirected toward savings and investment. It also improves your credit score, which can lower the cost of future borrowing. By taking a proactive approach to debt management, you’re not just getting rid of a burden. You’re taking a significant step toward financial freedom and a more secure future.

Setting Financial Goals

Setting financial goals is a powerful behavior that gives your financial decisions purpose and direction. When you establish clear, specific goals—whether short-term, like saving for a vacation, or long-term, like planning for retirement—you create a roadmap for your financial journey. Goals motivate you to stay disciplined, make informed choices, and resist the temptation to spend impulsively.

Financial goals also provide a sense of accomplishment as you achieve them, reinforcing positive financial habits. By regularly reviewing and adjusting your goals, you ensure that they remain aligned with your changing circumstances and priorities. Goal setting doesn’t mean just dreaming of a better future. It means actively shaping that future with every financial decision you make. This financial wellness helps you thrive in all other dimensions of your life..

Seeking Financial Education and Advice

Continuing to educate yourself and seeking professional advice are key behaviors that support long-term financial success. The financial world can be complex and ever-changing, making it essential to stay informed about new opportunities, risks, and strategies. By dedicating time to learning, whether through books, courses, or online resources, you empower yourself to make smarter, more confident decisions.

What’s more, seeking advice as needed from financial professionals can provide personalized guidance that helps you navigate specific challenges or opportunities. Whether you’re planning your investments, managing debt, or preparing for retirement, expert advice can offer clarity and insight that you might not gain on your own. By valuing financial education and advice, you’re investing in one of your most important assets: your financial well-being.

How Do You Overcome Behavioral Challenges?

Poor financial choices undermine consumers’ financial well-being and lead to financial stress, which diminishes overall quality of life. Understanding and addressing the behavioral challenges that drive these choices is key to improving your financial situation and overall happiness.

Identify Personal Financial Behavior Patterns

The first step in overcoming behavioral challenges is to identify your own financial behavior patterns. Take a close look at how you handle money on a day-to-day basis. Are there habits that consistently lead to overspending or financial stress? Perhaps you notice that you frequently make impulse purchases or avoid looking at your bank statements. These patterns often stem from deeper emotional or psychological triggers.

By becoming aware of these behaviors, you can start to understand what drives your financial decisions. This self-awareness is crucial because it allows you to see where changes are needed. Whether it’s tracking your spending more closely or setting up automatic savings, recognizing your patterns helps you take control of your financial life and make more deliberate, informed choices that support your well-being.

Recognize Common Behavioral Biases in Finance

Recognizing common behavioral biases is another crucial step in overcoming financial challenges. Biases like present bias, where immediate rewards outweigh future benefits, or loss aversion, where the fear of losing money is stronger than the motivation to gain it, often lead to poor financial decisions.

In the past, it was believed that people made financial choices purely based on logic, always aiming to maximize their financial gain. However, we now know that emotions and psychological biases play a significant role in these decisions. This means that even when we think we’re making rational choices, we might be influenced by our emotions or ingrained biases without realizing it. By understanding these biases, you can begin to see how they might be impacting your own financial decisions and take steps to counteract them.

Develop Strategies for Changing Negative Financial Habits

Once you’ve identified your patterns and recognized potential biases, the next step is to develop strategies for changing negative financial habits. This might involve setting up systems that make it easier to stick to your budget or finding ways to make saving more automatic and less dependent on daily willpower. For example, you could set up direct deposits into a savings account or use apps that round up your purchases and save the difference.

It’s also important to replace negative habits with positive ones. If you tend to spend impulsively, consider creating a 24-hour rule where you wait a day before making non-essential purchases. Or if you struggle with saving, start with small, manageable amounts and gradually increase them as you build the habit. The key is to create a plan that’s realistic and sustainable, so you can gradually shift your behavior in a way that supports your financial goals and reduces stress.

How Do You Build Positive Financial Habits?

Building positive financial habits is a crucial step towards achieving financial well-being. While understanding good financial behaviors is important, the real challenge lies in consistently implementing them. Fortunately, there are practical strategies you can employ to cultivate and maintain these beneficial habits. By incorporating these methods into your daily life, you can transform your financial behaviors and set yourself on a path to long-term financial success.

Create a Financial Routine

Establishing a consistent financial routine is a powerful way to build positive money habits. Start by setting aside specific times each week or month to focus on your finances. This could include reviewing your spending, updating your budget, or checking progress towards your financial goals. By making these activities a regular part of your schedule, you’re more likely to follow through and maintain good financial practices.

Your routine might involve a weekly check-in every Sunday evening to review your expenses and plan for the week ahead. Or you could schedule a more comprehensive monthly review where you assess your overall financial picture, including savings, investments, and debt repayment progress. The key is consistency – regular engagement with your finances helps reinforce good habits and keeps you accountable to your financial goals.

Automate Good Financial Behaviors

Automation is a powerful tool for building positive financial habits, as it removes the need for constant decision-making and willpower. By setting up automatic transfers and payments, you can ensure that you’re consistently saving, investing, and paying bills on time without having to remember or motivate yourself to do so each time.

Consider automating your savings by setting up a recurring transfer from your checking account to your savings account on payday. You can do the same for retirement contributions, ensuring you’re regularly investing in your future. Automating bill payments can help you avoid late fees and maintain a good credit score. By leveraging automation, you’re essentially programming good financial behaviors into your life, making it easier to stick to your financial plan and achieve your goals.

Use Technology to Support Positive Behaviors

In today’s digital age, there’s a wealth of technological tools available to support positive financial behaviors. Budgeting apps can help you track your spending and stay within your financial limits. Investment platforms can make it easier to diversify your portfolio and stay on top of your investments. Personal finance management software can provide a holistic view of your financial situation and help you make informed decisions.

Explore different apps and tools to find ones that align with your financial goals and preferences. For instance, you might use a app that rounds up your purchases to the nearest dollar and invests the difference, effortlessly building your savings. Or you could use a budgeting app that sends you alerts when you’re approaching your spending limits in various categories. By leveraging technology, you can reinforce positive financial behaviors and make managing your money more engaging and less daunting.

Remember, the key to successfully using these strategies is to find what works best for you. Experiment with different routines, automation strategies, and tech tools until you find a combination that feels sustainable and effective for your unique financial situation and goals.

What Is the Role of Financial Education in Shaping Behaviors?

Financial education gives you the skills and knowledge that lead to financial literacy. Financial education doesn’t have to take place in a classroom; any activity that increases your understanding or “skill” with money is a form of education.

Importance of Financial Literacy

Financial literacy is the ability to understand personal finance information and apply it, typically through financial decisions and behaviors. This foundational knowledge is crucial in today’s complex financial landscape, where individuals are increasingly responsible for managing their own financial well-being. With a solid understanding of financial concepts, you’re better equipped to make informed decisions about budgeting, saving, investing, and managing debt.

Financial literacy empowers you to ask the right questions, understand the implications of your financial choices, and navigate financial products and services with confidence. It can help you avoid costly mistakes, such as falling prey to predatory lending practices or making uninformed investment decisions. Moreover, financial literacy contributes to overall financial well-being by reducing stress associated with money management and increasing your ability to plan for both short-term and long-term financial goals.

Resources for Improving Financial Knowledge

Fortunately, there are numerous resources available to help you improve your financial knowledge. Many of these are accessible and often free, making it easier than ever to enhance your financial literacy. Public libraries often offer financial literacy workshops and materials. Online platforms (including ours) provide a wealth of information through courses, webinars, articles, and communities on various financial topics.

Government agencies, such as the Consumer Financial Protection Bureau, offer educational resources designed to help individuals make informed financial decisions. Financial institutions frequently provide educational content for their customers. Additionally, podcasts, books, and financial coaches and advisors can be valuable sources of information.

The key is to seek out reputable sources and to approach your financial education as an ongoing process, continuously expanding your knowledge as your financial situation evolves.

Financial Knowledge Guides Behavior in Real-life Situations

The true value of financial education becomes apparent when you apply your knowledge to real-life situations. Understanding concepts like compound interest can motivate you to start saving and investing earlier. Knowledge of credit scores and how they’re calculated can guide you in making decisions that maintain or improve your creditworthiness. Being familiar with different types of insurance can help you make appropriate choices to protect yourself and your assets.

In day-to-day life, financial knowledge can influence behaviors such as comparison shopping for the best deals, negotiating better terms on loans or credit cards, or recognizing and avoiding financial scams. It can also help you make more strategic long-term decisions, such as choosing the right mortgage, planning for retirement, or deciding how to fund your children’s education. By applying your financial knowledge to these real-world scenarios, you’re more likely to make choices that align with your financial goals and values, ultimately leading to improved financial outcomes.

Remember, financial education is not a matter of memorizing facts, but a matter of developing a mindset that allows you to approach financial decisions with confidence and clarity. As you continue to learn and apply your knowledge, you’ll likely find that your financial behaviors naturally align more closely with your long-term financial objectives.

Case Study: Overcoming Financial Challenges Through Behavioral Change

Meet Sarah and David, a couple in their late 40s who have recently found themselves grappling with financial dissatisfaction. Despite having steady careers, they’re burdened by car loans, a HELOC loan, and a mounting pile of credit card debt. More troubling for them is the realization that they’re far from achieving the retirement security they once envisioned. As they approach what they consider to be the peak of their earning potential, Sarah and David are stressed and uncertain about how to improve their financial situation.

Initially, they felt stuck, unsure of how to boost their income, and frustrated by their financial stagnation. But rather than letting this stress create distance between them, they began to talk more openly about their financial situation. These conversations were different from the occasional, surface-level chats they’d had before. This time, they dug deeper, sharing not only their frustrations but also their values, goals, and the underlying influences that shaped their financial behaviors. They discovered that many of their habits stemmed from early life experiences: Sarah’s tendency to spend as a way to combat stress, rooted in a childhood where money was tight, and David’s reluctance to invest, driven by his parents’ fear of financial risk.

As they continued to talk, a clearer picture of their financial behaviors emerged. With this new understanding, Sarah and David were ready to take action. They realized that while they couldn’t easily increase their income, they had significant control over how they managed their existing resources. Together, they devised a plan to improve their financial health by changing a few key behaviors.

First, they committed to tackling their debt more aggressively. They started by listing all their debts and creating a payment strategy that prioritized the highest-interest loans, such as their credit card debt. They decided to cut back on discretionary spending and redirect those funds toward debt repayment. By automating their payments and setting up regular reminders to review their progress, they stayed motivated and on track.

Next, they turned their attention to their long-neglected retirement savings. They began by adjusting their budget to increase their retirement contributions, even if only slightly at first. They also explored low-risk investment options that aligned with David’s comfort level, allowing them to gradually grow their retirement fund without feeling overwhelmed by market volatility.

In addition to these practical changes, Sarah and David embraced a more mindful approach to their spending. They started using a shared budgeting app to track their expenses and set realistic goals for saving and spending. This tool not only helped them stay accountable but also fostered a sense of teamwork as they worked toward their financial goals together.

As time passed, the positive impact of these behavioral changes became evident. Their debt began to shrink, their savings started to grow, and their conversations shifted from financial stress to financial progress. They no longer felt overwhelmed by their situation but instead experienced a growing sense of control and optimism about their financial future.

Now, having assessed their material assets, understood the psychosocial influences that shaped their behaviors, and made intentional changes to those behaviors, Sarah and David find themselves in a much better place. They have a clearer path toward a comfortable retirement and, most importantly, a renewed sense of financial well-being. By addressing the root causes of their financial dissatisfaction and making thoughtful changes, they’ve not only improved their finances but also strengthened their relationship and overall quality of life.

Financial behaviors play a pivotal role in shaping your overall financial well-being. As Lisa and Mark’s story illustrates, understanding and improving these behaviors can transform your financial outlook, reduce stress, and bring you closer to achieving your goals. By taking the time to assess your own financial habits and making deliberate changes, you can set yourself on a path toward greater security and peace of mind.

Key Takeaways

To recap the key points:

- Financial behavior is a crucial component of overall financial well-being, interacting closely with financial resources and psychology.

- Positive financial behaviors include budgeting, saving, investing, and debt management, while negative behaviors can hinder financial progress.

- Understanding personal values, goals, and influences is essential in shaping effective financial behaviors.

- Good financial habits compound over time, leading to significant improvements in financial well-being.

- Overcoming behavioral challenges and biases is possible through self-awareness and strategic planning.

- Financial education plays a vital role in guiding informed financial decisions and behaviors.

Remember, the journey to financial well-being is ongoing, and every step you take today brings you closer to a more secure and fulfilling future. Embrace the process, stay committed to your goals, and look forward to the positive changes that lie ahead. Much of your financial well-being is within your control, and by applying these proven behaviors over time, you can create the life you envision.

This post is part of a series that combines insights from psychology, personal finance, and holistic well-being. Together, these posts show how the synergy among these areas can elevate both your outlook and your financial bottom line. Whether you’re looking to better understand the situation of a friend, loved one, client or yourself, or whether you’re simply curious, you’ll find valuable insights and practical strategies throughout these articles. For a listing of these articles and convenient links to them, visit our series hub.

Resources

If you’d like to find out more about the behavioral side of financial wellness, including financial education and literacy, here are some valuable resources:

The Consumer Financial Protection Bureau offers practical personal finance tools, worksheets, handouts, and audio recordings.

On MyMoney.gov, you can find clear and straightforward explanations of the building blocks for managing and growing your money, as well as money calculators, checklists, and worksheets.

360 Degrees of Financial Literacy is a free public service offered by American CPAs to help people understand personal finance. Their site is easy to use and includes articles, videos, online financial calculators, and more.

The Federal Trade Commission offers a free simplified two-page worksheet to help you see where your money goes and plan next month’s spending.

Know Yourself, Grow Your Wealth is a set of free online programs designed by the American College of Financial Services to equip you with essential personal finance skills to boost your financial stability and set the stage for achieving your future financial goals.

Start or Join a Conversation

Thanks so much for your dedication to learning more about the psychosocial side of financial well-being.

Many different perspectives are possible about the behavioral side of financial well-being. Your thoughts are key to this community. Please share them here. If you don’t already have an opinion at the top of your mind, consider sharing your views on one of these points:

- What has been the most challenging financial behavior for you to change, and what strategies have you used (successfully or unsuccessfully) to address it?

- How have your childhood experiences or family attitudes towards money influenced your current financial behaviors? Have you had to unlearn any habits?

- Can you share a personal story of how a small change in your financial behavior led to a significant improvement in your overall financial well-being?

Do you have a question that wasn’t addressed in this post? Comment below, and I’ll give you my best answer.

And don’t forget to subscribe to our list to get updates about whole person finance.

Notice

This post is for educational purposes only and is not legal nor any other type of professional advice. You should consult your own attorney, financial advisor, health provider, or mental health professional concerning any issues in these areas of expertise. Please understand facts and views change over time. Posts reflect the author’s understanding at the time of writing, as well as the perspectives of external sources for this post. While maintained for your information, archived posts may not reflect current conditions.

Author Bio

Wendy helps people heal their relationship with money through a trauma-informed,

holistic approach. With a master’s in social work and years of experience as a social

worker, teacher, and financial well-being advocate, she brings deep insight from

both professional training and lived experience into the societal, relational, emotional, psychological, and somatic roots of financial behavior. She’s also the author

of Financial Trauma: Why Money Isn’t Just About Money, available here.

Your blog is a constant source of inspiration for me. Your passion for your subject matter is palpable, and it’s clear that you pour your heart and soul into every post. Keep up the incredible work!

Thanks for your encouraging words!